johndoe@gmail.com

Please find a PDF copy of this page here.

Name: Gaia Balp

Date: 21 December 2023

QUESTIONNAIRE ON DELISTING

Italy

The regulatory framework for delisting in Italy is set out in Legislative Decree No 58 of 24 February 1998 (Testo unico della Finanza (TUF) – hereinafter the ‘Consolidated Law on Finance (CLF)’ ), and in the Civil Code (CC). Regulations implementing the CLF are drawn by Consob, the Italian financial markets supervisory authority (Consob Regulation no 11971 of 14 May 1999 – hereinafter ‘Consob Issuer Regulation’ ). Provisions relevant to delisting from regulated markets are further included in the market rules set by Borsa Italiana, the Italian Stock Exchange (‘Regolamento dei mercati organizzati e gestiti da Borsa Italiana s.p.a.’ [Rules of the Markets Organized and Managed by Borsa Italiana], last amended on 24 July 2023, and approved by Consob on 11 September 2023 – hereinafter ‘Market Rules’ ). Provisions concerning delisting from MTFs are included in the Euronext Growth Milan market rules, equally set by Borsa Italiana. The overall regulation of Euronext Growth Milan is made of the following: Euronext Growth Milan General Provisions ; Rules for Companies (hereinafter ‘EGM Rules for Companies’); Rules for Euronext Growth Advisors ; Membership and Trading Rules ; Disciplinary Procedures and Appeals Handbook , and a number of associated implementing measures.

All answers, except answer to Q 21 and 36, refer to delisting from regulated markets.

PART I. VOLUNTARY DELISTING

A delisting is deemed voluntary if it is initiated by the company or a shareholder.

1. Is voluntary delisting explicitly allowed by national laws or by jurisprudence?

Yes No (X)

Relevant provision:

The only provision explicitly allowing voluntary delisting from regulated markets (irrespec-tive of ‘cold’ delisting, on which see answer to Q 18 below) is that referred to market mi-gration, enshrined in Article 133 CLF (see answer to Q 15 below).

Differently from other jurisdictions such as Germany (§ 39 BörsG; II ZR 133/01 ‘Macrotron’) and the UK (LR 5.2), Italian law explicitly regulates voluntary delisting only where it is asso-ciated with market migration.

In effect (and beyond Article 133 CLF on market migration), Article 2437-quinquies Civil Code grants shareholders an exit right upon delisting from regulated markets (on which see answer to Q 13 below). The right to withdraw from the company applies for share-holders who ‘did not contribute to the decision that determined delisting’. The wording of Article 2437-quinquies (as well as of previous provisions, no more in force, from which Article 2437-quinquies derives) justifies the view according to which decisions that trigger the right to withdraw refer not to resolutions whose very object is delisting itself, but those (such as a merger into a non-listed company) that, having some other measure as the direct object, only indirectly determine delisting. The rules on mandatory delisting (removal from trading following a decision by the market operator pursuant to Article 66-ter CLF, on which see answer to Q 24 below) do not either explicitly include any provision that the issuer may request the market operator to remove a financial instrument from trading.

Therefore, voluntary delisting as the decision made by the company itself, to exit the market (‘pure’ delisting), remains unregulated, and the very legitimacy of pure delisting is still not undisputed, in spite of the permissive stance taken by the doctrine now prevailing (according to which, amongst further reasons: the wording of Article 2437-quinquies CC is not decisive, and prevents not a less strict interpretation; Article 66-ter CLF does not explicitly prevent (hence implicitly admits) an issuer’s request for voluntary pure delisting).

Given the uncertainty still surrounding the legitimacy of pure delisting under national law, voluntary delisting initiated by a shareholder or the company can be achieved, and is actually achieved in the practice, indirectly, through a transaction for the purchase of a number of shares such as to eliminate the requirements for maintaining the listing (reduction of free float below the minimum threshold required by market regulation, most often achieved by means of a takeover bid) or a transaction following which the issuer itself is extinguished (merger into a non-listed company): see answer to Q 18 below on cold delisting.

2. If the answer to 1. is yes, who decides so?

BoD GA Other (X)

Relevant provision:

Article 133 CLF

Where the request for delisting is motivated by market migration (see answers to Q 1 above and Q 15 below), a resolution by the extraordinary shareholders' meeting of the migrating company is explicitly required by article 133 CLF.

Where pure delisting (a decision made by the company to abandon the market) is deemed to be implicitly admitted under Italian law (see answer to Q 1 above), the corresponding resolution is certainly to be made by the extraordinary shareholders meeting. This conclusion plainly derives from Article 133 CLF (regulating market migration): if market migration requires a resolution made by the extraordinary shareholders’ meeting, all the more reason for the same requirement to apply where voluntary delisting leads not just to trading on a different (regulated) venue, but to no trading at all, thereby affecting the liquidity of the investment much more deeply. Hence, Article 133 CLF analogically applies to pure delisting.

3. What is the quorum requirement for the delisting decision of the competent organ?

As a general rule, Article 2369(7) Civil Code sets the quorum requirement for listed companies’ extraordinary shareholders’ meetings at 20 per cent of the share capital granting voting rights. Under Article 2369(1), the articles of association may however choose to adopt a system based on multiple calls for extraordinary shareholders’ meetings (call 1: 50 per cent of the share capital granting voting rights; call 2: 1/3 of the share capital granting voting rights; call 3 (and further calls): 20 per cent of the share capital granting voting rights).

4. What is the majority requirement for the delisting decision of the competent organ?

The majority requirement provided for by Article 2369(7) Civil Code for listed companies’ extraordinary shareholders’ meetings is 2/3 of the share capital (granting voting rights) represented at the meeting.

5. Do (minority) shareholders have statutory veto rights as to a delisting decision?

Yes No (X)

Minority shareholders are not given any veto rights in regard to delisting (they instead are granted an exit right). However, the fact that market migration (and pure delisting: see above) requires a decision by the extraordinary shareholders’ meeting (see answer to Q 2 above) entails that, depending on the circumstances, organized, active minorities (typically institutional shareholders) collectively holding a non-negligible proportion of voting rights may succeed – at least theoretically – in successfully opposing the proposal: see answers to Q 3 and 4 above.

6. Should delisting take place within a specific timeframe after the relevant decision? Is there a specific period of time after the decision in which the delisting should be completed?

Yes (X) No

Relevant provision:

Article 144(1) Consob Issuer Reg.

Regarding market migration (Article 133 CLF, on which see answer to Q 15 below), Article 144(1) of Consob Issuer Reg. provides that ‘The rules of a market shall discipline removal from trading upon request pursuant to Article 133 CLF and shall also establish an adequate period of time, of no less than one month, between the decision to request removal from trading and the date of effective removal’. The ‘rules of the market’ mentioned in Article 144(1) are those laid down in Articles 2.5.5 and 2.5.6 of the Market Rules, and in the accompanying Instructions of the market operator (on which see answers to Q 7 below).

7. Should the delisting application give a full statement of reasons for the submission of such application?

Yes (X) No

Relevant provision:

Article 2.5.5 Market Rules

In the case of market migration (Article 133 CLF), Article 2.5.5(1) of the Market Rules requires that ‘Italian issuers with shares listed on the Euronext Milan or Euronext MIV Milan market shall send Borsa Italiana a written request drawn up in conformity with the model contained in the Instructions and signed by the legal representative’. Attached to the application, the issuer is required to submit a) the resolution of the extraordinary shareholders’ meeting to request delisting; b) the declaration of admission to listing on another regulated market in Italy or another EU country (see Article 2.5.5(2) of the Market Rules).

The model form provided in the Instructions (‘Instructions accompanying the rules of the markets organized and managed by Borsa Italiana s.p.a.’ ) does not require the issuer to (further) explain the reasons for delisting, given that such reasons are already given in the minutes of the shareholders’ meeting that made the decision, which are to be attached to the application.

The very same reasonably applies in the case of a company’s application for pure delisting.

8. Is it required that a competent authority approves the voluntary delisting? If the answer to 8 is yes: who is the competent authority? Does the competent authority have the competence to verify the reasons of delisting? Does the competent authority have any discretion? Can the competent authority impose additional terms for investor protection? Can the competent authority postpone the decision? If Yes, do you know whether this discretion has been used in the past?

Yes (X) No

Relevant provision:

indirectly, Articles 66-ter and 66-quarter CLF

In spite of the absence of any rule disciplining pure delisting, it is reasonable to assume that, in all circumstances in which the market operator exercises its power to remove securities from trading beyond the scope of application of Articles 52 and 69 MiFID II (on which see answers to Q 22 and 24 below), an initiative by the issuer itself, hence a request, is required. It is however evident that, in such cases, removal from trading does not automatically follow the issuer’s request. The final decision is vested with the market operator after verifying that the necessary conditions are met, in particular those regarding the interests of the investors and the orderly functioning of the market.

9. In case of a voluntary delisting does the issuer have to make an offer to buy the shares of (dissenting) shareholders?

Yes No

N.A.

If the answer to 9 is yes, at what price should the offer be made? How is the price calculated?

See answers to Q 13 and 18–20 below.

10. Are there any restrictions due to the principle of maintenance of the share capital?

Yes No

N.A.

Note, however, that capital maintenance-motivated restrictions usually imposed on share buy-backs do not apply where buy-backs are the consequence of a merger. See Article 2357-bis (1)(4) (‘Special cases of purchase of treasury shares’), under which ‘limitations set by Article 2357 do not apply when the purchase of treasury shares occurs … as a result of universal succession, merger or demerger’.

11. Does a (majority) shareholder or a third person has the right to offer to buy the shares of (dissenting/all) shareholders and relieve the issuer?

Yes No

N.A.

12. In case of a voluntary delisting does the issuer or a third person have the obligation to publish a prospectus / informational document?

Yes No

N.A.

Where voluntary delisting is the consequence of a takeover bid, or a merger, the relevant information is to be published in the prospectus/information document required by the corresponding discipline.

13. Is an exit opportunity/ mechanism that allows investors to exit their investments (e.g. sell-out right) available for shareholders in case of delisting? What are the relevant provisions (please provide translations)?

Yes (X) No

Relevant provision:

Article 2437-quinquies Civil Code

In the case of ‘cold’ delisting (see answer to Q 18 below), and of pure delisting as well (where deemed possible: see answer to Q 1 above), Article 2437-quinquies Civil Code applies, under which shareholders (holding listed equities) who ‘did not contribute to* the decision that determined delisting**’ are granted the right to withdraw from the company.

* abstaining/dissenting shareholders

** decisions that typically determine delisting (ie where delisting is a consequence of, and therefore ensues, such decisions) are those concerning mergers)

Upon withdrawal, the shareholder is paid a value equal to the average market price of the shares in the last 6 months before publication of the notice of call of the shareholders meeting (see Article 2437-ter(3) Civil Code ). Therefore, shareholders are granted an exit at a value unaffected by delisting.

Where pure delisting is considered legitimate under Italian law (see answer to Q 1 above), Article 2437-quinquies Civil Code, and the associated safeguards regarding the value of the shares to be paid to withdrawn shareholders, are deemed to apply as well.

Shareholders are granted further exit opportunities in connection with takeover bids, and the associated sell-out and squeeze-out rights laid down in Articles 108 and 111 CLF: see answers to Q 18–20 below.

14. Is there any specific provision on downlisting? If not, is downlisting allowed, and how does it take place?

A downlisting occurs when the shares are no longer traded on a regulated market (as defined by Union law) but on an MTF.

Yes No (X)

Relevant provision:

Article 133 CLF (see answer to Q 15 below) does not apply to downlisting, since it only covers migration to a another (Italian or European) regulated market, ie to a trading venue offering the same characteristics and safeguards as the original venue. Hence, under Italian law, downlisting requires a two-step process, each regulated by its own rules: 1) delisting; 2) admission to listing on an MTF.

15. Is there any specific provision on market migration (delisting from a regulated market and listing in another)?

Yes (X) No

Relevant provision:

Article 133 CLF (‘Removal from trading upon request’) provides that ‘Subject to approval by an extraordinary shareholders' meeting, Italian companies with shares listed on regulated markets in Italy may request that their own financial instruments be removed from trading, in accordance with the provisions of the rules of the market, where they are admitted to listing on other regulated markets in Italy or another Member State, provided that investors are ensured equivalent protection, according to standards established by Consob in a regulation.’

(See also Article 144(2) Consob Issuer Reg., under which ‘Removal from trading of ordinary shares shall be subject to the existence in the market where the shares are listed of provisions on mandatory take-over bids that are applicable to the issuer in the event of the transfer of controlling holdings or to the existence of other conditions deemed equivalent by CONSOB.’)

16. Is there any specific provision on voluntary delisting in case of increase of listing requirements by both the Law and Stock Exchange?

Yes No (X)

17. Are there different rules on delisting for national and foreign listed companies?

Yes (X) No

Relevant provision:

Article 133 CLF: Article 2.5.6 Market Rules

The scope of application of Article 133 CLF (see answers to Q 1 and 15 above) is narrow, since it only applies to “Italian companies with shares listed on regulated markets in Italy”. Hence, differently from equivalent provisions on market migration set forth in other jurisdictions (eg, § 39(2) BörsG), Article 133 does not apply to companies established in other Member States, whose shares are traded on Italian regulated markets. Article 133 neither applies to migration to a non-EU regulated market.

However, a market rule applicable to foreign companies was adopted by the stock ex-change. Specifically, Article 2.5.6 of the Market Rules essentially duplicates for foreign companies the provisions of Article 133 CLF, except for the requirement of a resolution by the extraordinary shareholders’ meeting (the identification of the competent organ is left to the relevant national law).

18. Cold delisting is usually described as a transformation of a listed company resulting to its delisting, including especially the merger by absorption of a listed company by an unlisted company. What is defined as cold delisting in your legal order? Is there any specific provision on cold delisting?

Cold delisting is a definition not as usual in Italy as it is in Germany. In Germany, the term ‘kaltes Delisting’ refers to a delisting caused by some major, structural corporate transaction, such as a merger, following which the prerequisites for listing are no longer met.

Under Italian law, delisting caused by major corporate or market transactions that negatively affect the tradability of a company’s securities, or the level of free float (thereby preventing securities from continuing to be listed), fall within the remit of Article 66-ter CLF (regulating the decision by the market operator to remove such securities from trading: see answer to Q 24 below). Although in such cases delisting formally follows a decision by the market operator (due to the impossibility to maintain the market’s orderly functioning), from a substantive point of view delisting can actually be regarded as the consequence of a decision made by the company itself, or by a shareholder, which upon making such determination also makes public the intention to abandon the market.

Transactions that lead to delisting in Italy typically include mergers, as well as (mandatory or voluntary) takeover bids and sell- and squeeze-outs (disciplined under Articles 111 and 108 CLF*). In the case of sell-out, delisting ensues the decision of the shareholder (or shareholders acting in concert) holding more than 90 per cent of the share capital (or 95 per cent, where the threshold is reached following a global takeover bid) not to restore an adequate level of free float, following which such shareholder/s is/are under a legal obligation to buy the remaining listed securities from any holder thereof that requires so. Article 2.5.1 (6)** of the Market Rules provides that securities subject to sell-out under Article 108 CLF are removed from trading, unless the majority shareholder has declared its willingness to restore the free float.

*Article 108(2) CLF (on sell-out) provides that any party becoming holder of more than 90 per cent of the shares admitted to trading on a regulated market, shall be committed to buy the remaining securities admitted to trading from any holder thereof requiring so unless a free float adequate to ensure orderly trading is restored within 90 days.

Article 108(1) CLF (on sell-out) further provides that any party who, upon completion of a global take-over bid, becomes the holder of at least 95 per cent of the shares admitted to trading on a regulated market, shall be committed to buy the remaining securities admitted to trading upon request by any holder thereof.

Article 111 CLF (on squeeze-out) provides that “A bidder who, following a global takeover bid, becomes holder of at least 95 per cent of the voting shares in an Italian listed company shall have the right to buy the remaining securities within three months from reaching the said threshold, if the intention to exercise said right was declared in the takeover bid document”.

** Article 2.5.1 (6) Market Rules:

“Where there is a purchase obligation pursuant to Article 108, paragraphs 1 and 2, of the Consolidated Law on Finance, the securities that are the subject of the legal purchase obligation shall be delisted and withdrawn from trading as of the trading day following the last day for the payment of the consideration, unless the person under the obligation pursuant to Article 108, paragraph 1, of the Consolidated Law on Finance has declared that he intends to restore the free float. Where the conditions referred to in Article 111 of the Consolidated Law exist, the securities that are the subject of the legal purchase obligation shall be suspended and/or delisted and withdrawn from trading, taking into account the timetable for the exercise of purchase right. Borsa Italiana shall notify the market the date of the revocation appropriately in advance.

In the case referred above, moreover, Borsa Italiana may at the same time revoke the listing and trading of all the non-voting shares, where there is an offer for all these shares, taking into account the value of their remaining free float.”

19. Does the merger of a listed company with a non-listed company lead to delisting? Is an exit opportunity available for shareholders? What are the relevant provisions? (please provide translations)

Yes (X) No

Relevant provision:

See answer to Q 18 and 13 above.

20. Does the successful completion of a mandatory bid give the right to delisting? If yes, are there any preconditions?

Yes (X) No

Relevant provision:

Article 111 CLF

Under the squeeze-out rule (see answer to Q 18 above), the right to forcefully buy-out the remaining shares is granted the bidder upon completion of a takeover bid (either mandatory or voluntary) launched on 100 per cent of the voting shares traded (global takeover bid), following which the bidder reaches a stake of no less than 95 per cent of the voting rights. The squeeze-out right is granted provided that the bidder has declared his intention to exercise such right.

21. Are there specific rules on delisting from an MTF?

Rules on delisting from an MTF are not provided in the law, but in the Euronext Growth Milan Rules for Companies. Specifically, under Article 41 on cancellation,

[a]n Euronext Growth Milan company wishing Borsa Italiana to cancel admission of its Euronext Growth Milan securities must notify such intended cancellation, also informing the Euronext Growth Advisor, and must separately inform Borsa Italiana of its preferred date for cancellation at least twenty business days prior to such date and, unless Borsa Italiana decides otherwise, cancellation shall be conditional upon the consent of no less than 90% of the votes cast by its shareholders in a general meeting. […] Cancellations are effected by a dealing notice.

Therefore, pure delisting from an MTF is allowed upon meeting a supermajority requirement.

Schedule Six of the EGM Rules for Companies requires that a mandatory, predefined can-cellation clause be included in the bylaws of any Euronext Growth Milan company. Under such clause,

[a] Company which wishes Borsa Italiana to cancel admission of its Euronext Growth Milan securities must notify such intended cancellation, also informing the Euronext Growth Advisor, and must separately inform Borsa Italiana of its preferred cancellation date at least twenty trading days prior to such date. Without prejudice to the exemptions provided in the Euronext Growth Milan Rules, the request must be approved by the shareholders' meeting of the Euronext Growth Milan Company by a majority of 90% of the participants. This resolution quorum shall apply to any resolution of the Euronext Growth Milan Company that may result, even indirectly, in the exclusion of Euronext Growth Milan securities from trading, as well as any resolution to amend this bylaw provision.

While Article 41 of the EGM Rules for Companies only explicitly refers to pure delisting, the cancellation clause required by Schedule Six clarifies that the supermajority requirement applies to any resolution directly or indirectly determining delisting, hence including decisions such as a merger. Indirect voluntary delisting is therefore also included.

Article 41 of the Rules does not clarify whether the delisting resolution is to be made by the ordinary, or the extraordinary, shareholders' meeting. However, since such resolution can significantly affect the organizational structure of the company, it is fair to assume that delisting from non-regulated markets requires a resolution made by an extraordinary shareholders’ meeting.

Importantly, based on the wording of Article 2437-quinquies CC, withdrawal (on which see answer to Q 13 above) does not apply to delisting from an MTF as a means of minority shareholder protection; in fact, Article 2437-quinquies CC only refers to delisting from regulated markets. Some doctrine yet considers that Article 2437-quinquies should analogically apply to delisting from MTFs as well.

EGM Rules for Companies further provide that a mandatory takeover clause, as predefined in Schedule 6, be included in the bylaws of any EGM issuer. Under such clause,

[f]rom the time the Company’s shares are admitted to trading on Euronext Growth Milan, the provisions on mandatory cash and exchange tender offers on listed companies referred to in Legislative Decree 58/1998 and the related Consob implementing regulations, limited to the provisions referred to in the Euronext Growth Milan Rules for Companies, shall become applicable by voluntary reference and insofar as they are compatible.

Furthermore, Article 6-bis of the EGM Rules for Companies provides that, where an Euronext Growth Milan issuer becomes the target of a takeover bid, the rules set out in the CLF (and related implementing provisions and Consob guidelines) shall apply (by voluntary references in the bylaws) as regards:

- the thresholds triggering the mandatory offer (see Article 106 (1), (1-bis), (1-ter), (3)(a), (3)(b), (3-bis), (3-quarter) CLF; Articles 44-bis, 44-bis.1, 44-ter, 45, 46 Consob Reg.);

- exemptions from the mandatory offer (see Article 106 (4), (5), (6), CLF; Article 49, Consob Reg.);

- the identification of those required to launch the offer (see Articles 106 (1) and (2), and 109 CLF; Article 44-quater Consob Reg.);

- the conditions (price and consideration) and time arrangements for the mandatory offer (see Article 106 (1), (2), (2bis), and (3)(c-d) CLF; Articles 40 (2)(b), and, limited to the cases of price increase and reduction at the request of those interested, Articles 47-bis, 47-ter, 47-quinquies, 47-sexies, 47-septies, 44-octies, Consob Reg.).

Finally, under Article 6-bis of the EGM Rules for Companies, even if not required by law, offerors must publish an information document drawn up in accordance with the forms provided by Schedule 2A of Consob Issuer Reg., bearing, in a prominent position and printed in bold type, the following sentence: ‘Neither Consob nor Borsa Italiana have approved the contents of this document.’

Further provisions included in Article 6-bis of the EGM Rules for Companies refer to the independent panel appointed by Borsa Italiana and entrusted with making decisions in relation to mandatory takeover bids pursuant to Rule 6-bis, including the making of any rulings appropriate or necessary for the correct execution of the offer. Such rulings are to be made based on the CLF provisions mentioned above, as well as those referred to: relevant definitions (Article 101-bis (4), (4-bis) and (4-ter) CLF and Article 35 Consob Reg.); publication of notices and documents pertaining to the offer (Articles 102 (1) and 103 (4)(a) CLF and Article 36 Consob Reg.); the offeror’s communication (Article 102 (1) CLF, and Article 37 Consob Reg.) and guarantees (Article 37-bis (1) Consob Reg.); implementation of the offer (Article 103, (1) and 4(a), CLF and Article 40 Consob Reg.); transparency and correctness (Article 103, 4 (b) and 4(c) CLF; Articles 41 and 42 Consob Reg.); amendments to the offer and competing offer (Article 103 (4)(d) CLF; and Articles 43 and 44 Consob Reg.).

PART II. OBLIGATORY DELISTING

A delisting is deemed compulsory/obligatory, if it is initiated by a supervisory authority or a market operator without consent of the company.

Mandatory delisting, which is associated with market protection, may be decided by either Borsa Italiana (the market operator) under Article 66-ter CLF, or by Consob (the supervisory authority) under article 66-quater CLF. Articles 66-ter and 66-quater CLF directly stem from EU law (Articles 52 and 69(2) MiFID II), in order to limit a market operator’s discretion in regard to the sensitive decision to remove securities from trading.

22. What are the prerequisites for compulsory delisting by the competent national supervisory authority?

Under Article 66-quater CLF, Consob may directly suspend or remove financial instruments from trading (market operator inertia hypothesis), or request that the market operator does so.

Where the market operator (suspends or) removes a financial instrument from trading (pursuant to article 66-ter CLF: see answer to Q 24 below), Consob orders that the other market operators and systematic internalizers that trade the same financial instrument also (suspend or) remove it from trading, if (suspension or) removal is due to suspected market abuse, a takeover bid, or failure to make public inside information about the issuer or the financial instrument in breach of Articles 7 and 17 MAR, unless said (suspension or) removal could damage the interests of the investors or the orderly functioning of the market. The same applies where a financial instrument is (suspended or) removed from trading based on a decision by competent authorities of other Member states.

23. Which body has been designated as the competent authority, in particular regarding the power to require the removal of a financial instrument from trading pursuant to art. 69(2)(n) MiFID II?

Consob (see answer to Q 22 above).

24. What are the rules of the market that can justify a compulsory delisting imposed by market (art. 52 of Directive 2014/65)?

Under Article 66-ter CLF the market operator ‘may remove the financial instruments from trading where such financial instruments cease to comply with the rules of the market, unless said exclusion would be likely to cause significant damage to the interests of the investors or the orderly functioning of the market.’ The market operator makes public the decision on removal, and immediately communicates it to Consob.

In the case of regulated markets, Consob may however prohibit the enforcement of any decision of removal from trading within five open market days from receipt of the communication from the market operator if, based on information different from that assessed by the market managing the course of its discovery, it considers such decision contrary to the purpose of ensuring transparency, orderly trading and investor protection. Execution of the decision to remove shares from trading is therefore suspended until a 5-days term elapses.

As to the merits of the market operator’s decision to remove securities from trading, Arti-cle 2.5.1(1)(b) of the Market Rules provides that ‘Borsa Italiana may revoke the listing and trading of a financial instrument in the event of a prolonged lack of trading or where it deems that, owing to special circumstances, maintain a normal and regular market for such instrument is not possible.’

Under Article 2.5.1(5) of the Market Rules, for the purposes of removal from trading the market operator shall consider primarily the following circumstances:

a) the average daily turnover in the market and the average number of securities traded over a period of at least eighteen months; b) the frequency of trading in the same period; c) the distribution among the public of the financial instruments in terms of value and number of holders; d) the involvement of the issuer in insolvency proceedings; e) an adverse opinion by the statutory auditor or the statutory auditing company or a disclaimer rendered by the statutory auditor or the statutory auditing company for two consecutive financial years. f) the liquidation of the issuer; g) suspension from trading for a period of more than 18 months.

Where delisting ensues the exercise of squeeze-out and sell-out rights (see answer to Q 18-20 above), Article 2.5.1(6) of the Market Rules applies, according to which:

Where there is a purchase obligation pursuant to Article 108, para. 1 and 2, CLF, the securities that are the subject to the legal purchase obligation shall be delisted and withdrawn from trading as of the trading day following the last day for the payment of the considera-tion, unless the person under the obligation pursuant to Article 108, para. 1, CLF has declared that he intends to restore the free float. Where the conditions referred to in Article 111 CLF exist, the securities subject to the legal purchase obligation shall be suspended and/or delisted and withdrawn from trading, taking into account the timetable for the exercise of purchase right. Borsa Italiana shall notify the market the date of the revocation appropriately in advance.

In the case referred above, moreover, Borsa Italiana may at the same time revoke the listing and trading of all the non-voting shares, where there is an offer for all these shares, taking into account the value of their remaining free float.

The procedure disciplining removal from trading is laid down in Article 2.5.2 of the Market Rules, according to which:

1. Borsa Italiana shall send the issuer a written notification setting out the elements that constitute the grounds for revocation and establishing a time limit of no less than 15 days for the submission of written briefs.

2. In such briefs the issuer may request a hearing. Borsa Italiana may also request a hearing where it deems this necessary. The hearing shall be attended by the legal representative of the issuer or a person specifically appointed. Where the issuer fails to attend the hearing without good reason, Borsa Italiana shall proceed on the basis of the elements in its possession.

3. Borsa Italiana shall decide within 60 days of the transmission of the notification referred to in para. 1.

4. The time limit of 60 days may be interrupted once by means of a notification by Borsa Italiana where it considers it necessary to request additional data and information on significant events that occurred after the start of the revocation procedure. In this case the time limit of 60 days shall start again from the date of receipt of the information requested.

5. The start of the revocation procedure shall be immediately notified to Consob.

25. Have any of the voluntary or obligatory delisting requirements above changed materially since 2010 (e.g., due to a legal decision or amendment of the regulations)?

No.

PART III. GENERAL QUESTIONS (if not already answered)

26, How are dissenting shareholders protected in voluntary delisting?

See answers to Q 2, 13, and 18–20 above.

27. What are the sanctions in case of a breach of the delisting rules?

28. Is there a special duty of loyalty (for the board or, if applicable, the shareholders) imposing further restrictions in connection with a delisting?

29. How are shareholders protected in obligatory delisting?

See answers to Q 22–24 above.

30. Have shareholders successfully challenged delisting decisions in the past? If Yes, could you provide any names of cases?

31. How is the issuer protected in (obligatory) delisting?

See answer to Q 22 above.

32. How does insolvency and restructuring of a listed company affect delisting? Specifically: a) Does the initiation of formal insolvency (liquidation) procedures automatically trigger mandatory delisting? b) Does the initiation of formal restruc-turing/ reorganization procedures automatically trigger mandatory delisting? c) If the above scenarios do not automatically trigger mandatory delisting, what else are the implications? d) Please give empirical information (if available) on the treatment of insolvent listed firms by trading venues in your jurisdiction e) What are the relevant provisions (please provide translations)?

Insolvency proceedings are among the circumstances the market operator is to take into account for the purposes of both removal (see answer to Q 24 above) and suspension from trading. See Article 2.5.1(2) of the Market Rules, according to which

For the purposes of the suspension of trading referred to in the preceding paragraph, Borsa Italiana shall refer primarily to the following elements:

a) the dissemination or lack of dissemination of information that may affect the regular operation of the market; b) the adoption of a resolution reducing the share capital to zero and simultaneously increasing it above the legal limit; c) the involvement of the issuer in insolvency proceedings; d) the liquidation of the issuer: e) an adverse opinion by the statutory auditor or the statutory auditing company or a disclaimer rendered by the statutory auditor or the statutory auditing company for two consecutive financial years.

33. Do relevant courts have the power to examine the delisting reasοns on the merits?

34. What are the legal consequences of delisting: a) on shares, b) on shareholders, c) on the issuer?

35. Are there any statistical data on delisting in your Country? If yes, please provide further details. Are there any statistical data, or evidence, on downlisting in your Country? If yes, please provide further details. Are there any statistical data, or evidence, on delisting from an MTF in your Country? If yes, please provide further details.

See answer to Q 36 below. No data on downlistings available.

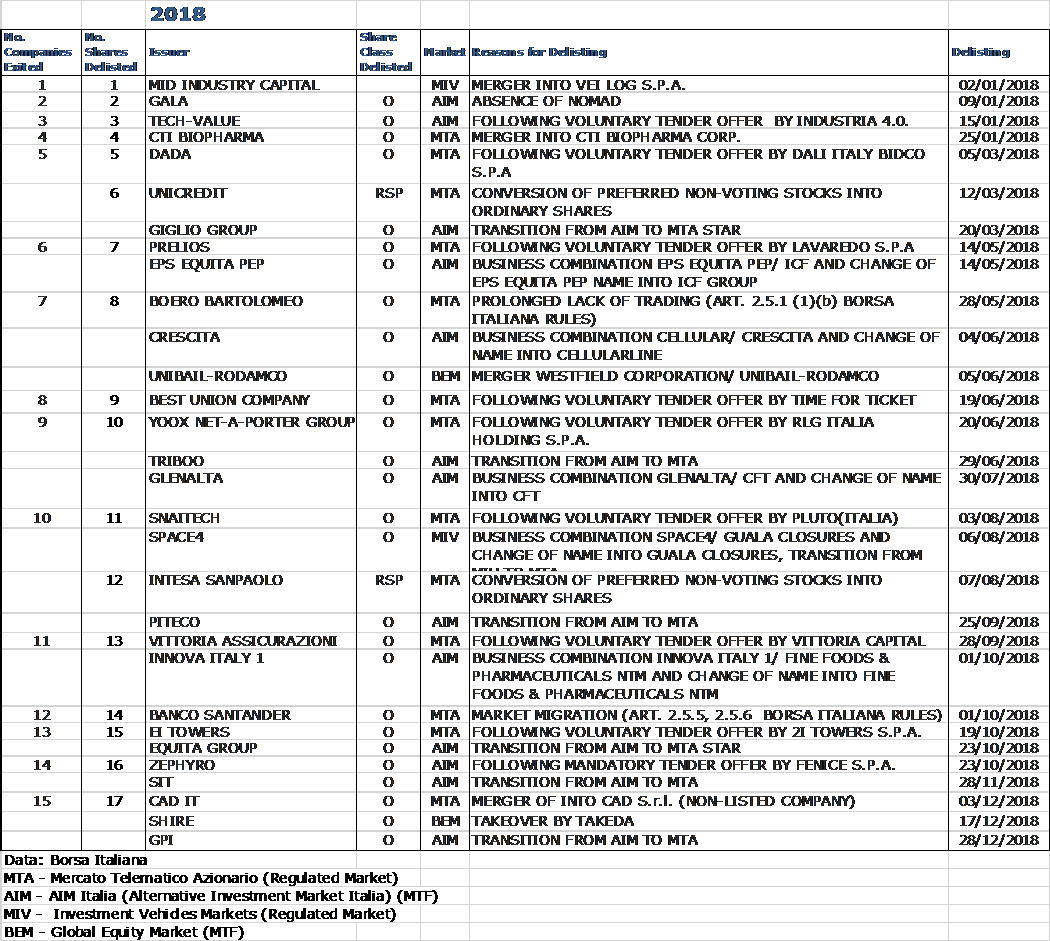

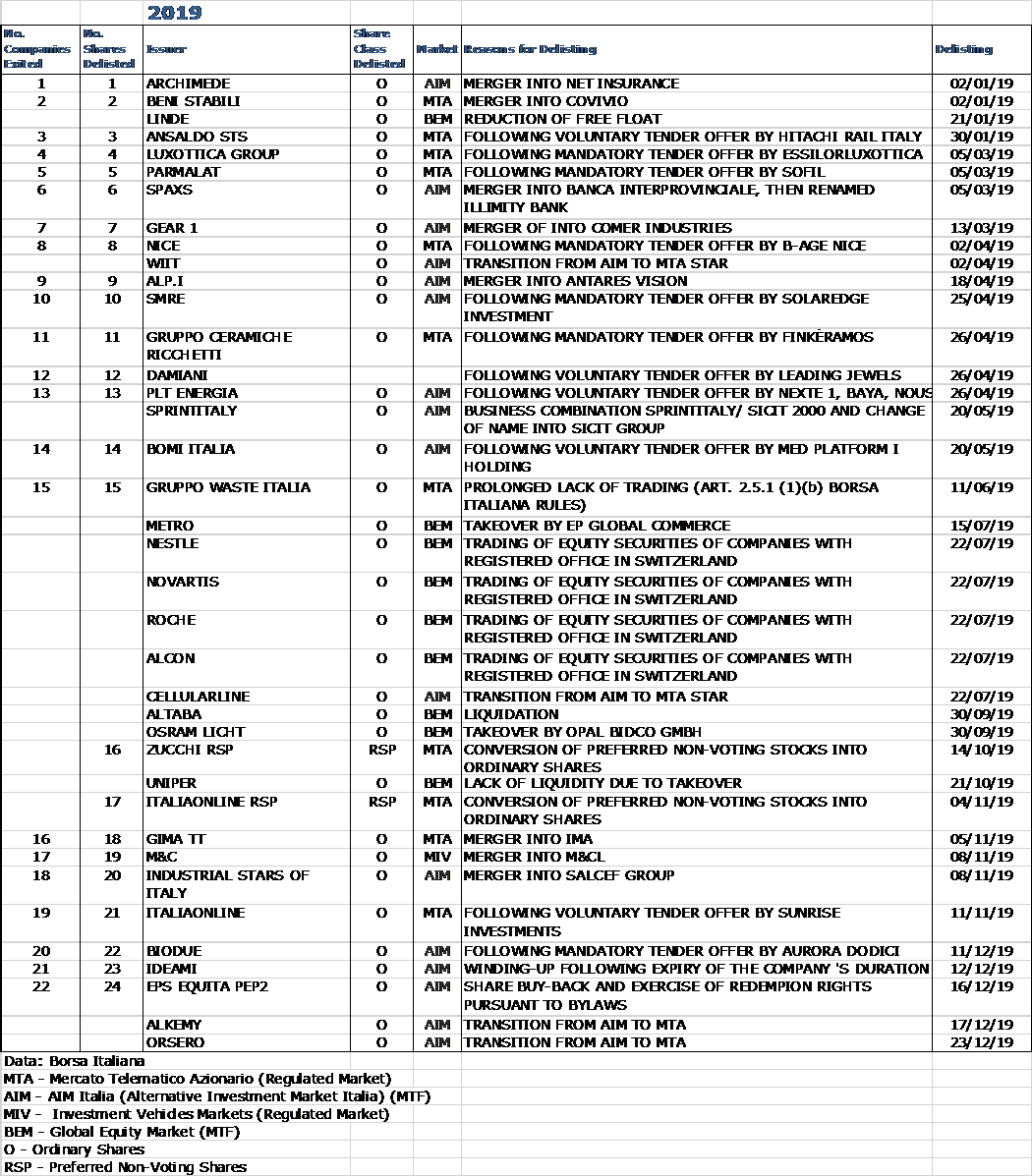

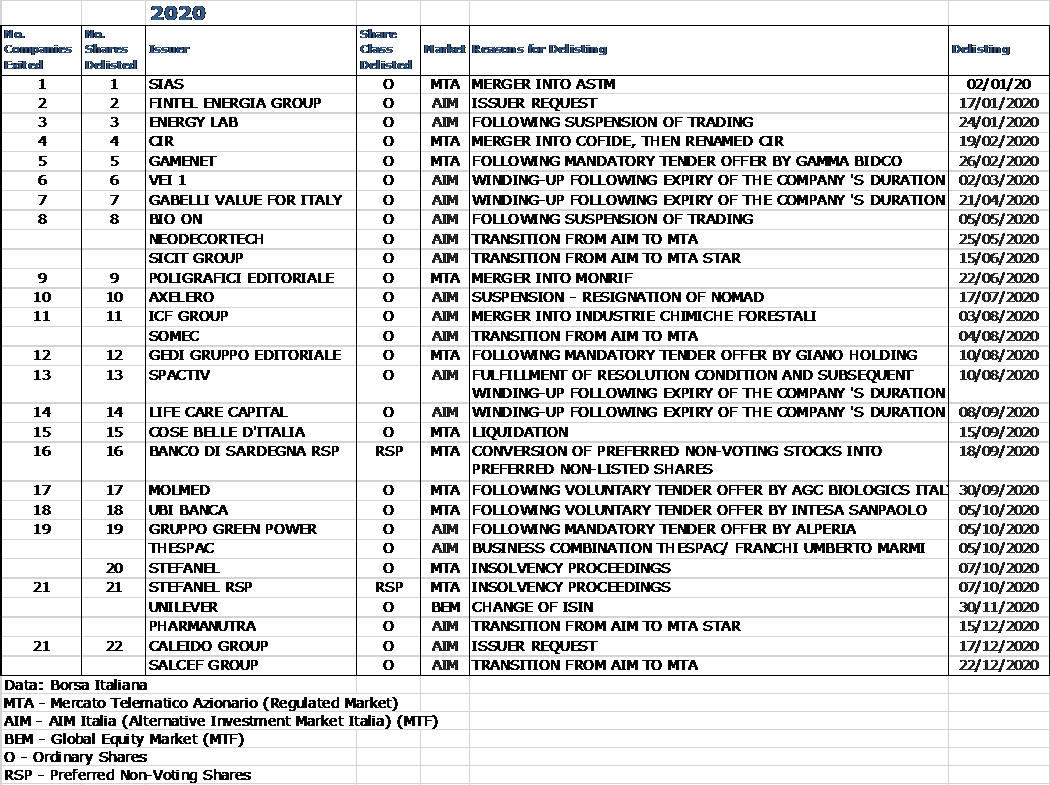

36. More specifically, how many cases of voluntary delisting and/or obligatory delisting by the competent national supervisory authority have there been since MiFID I entered into force in 2007? Please also provide the main reasons for mandatory delistings, if available.

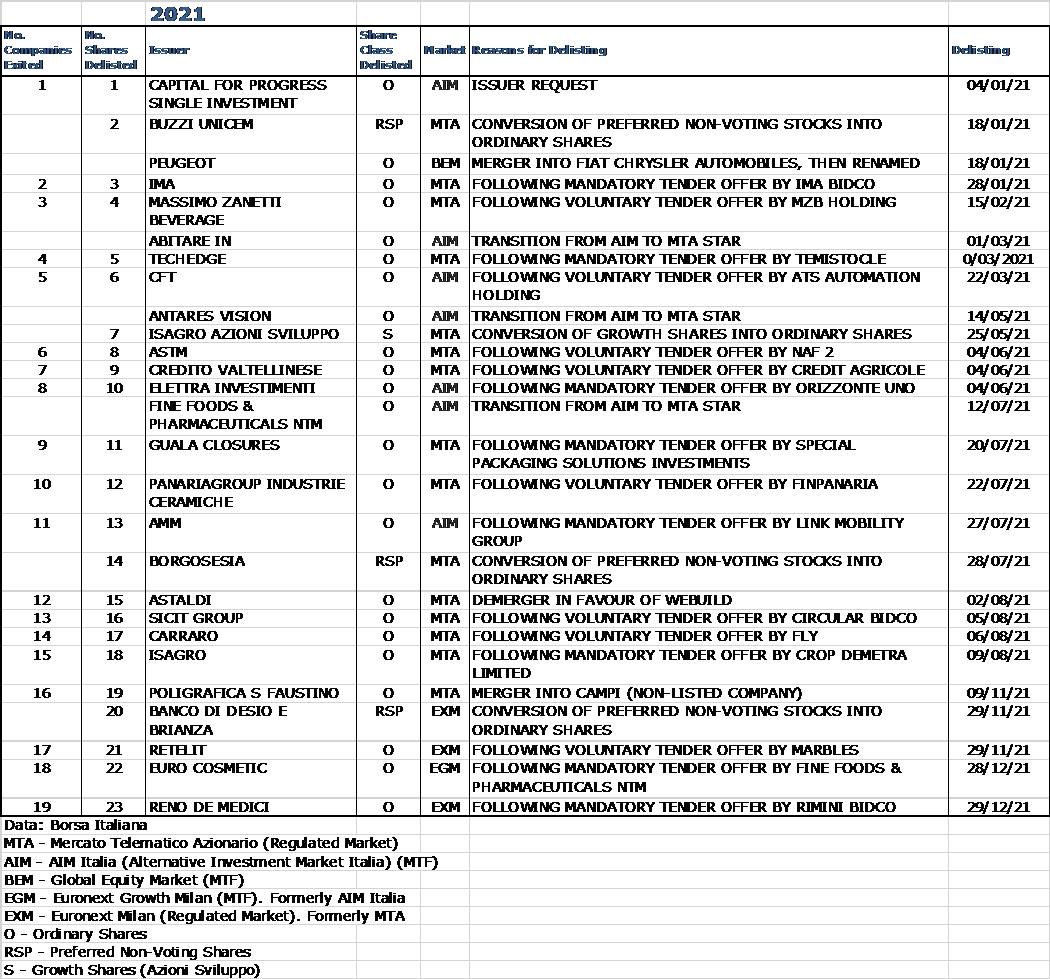

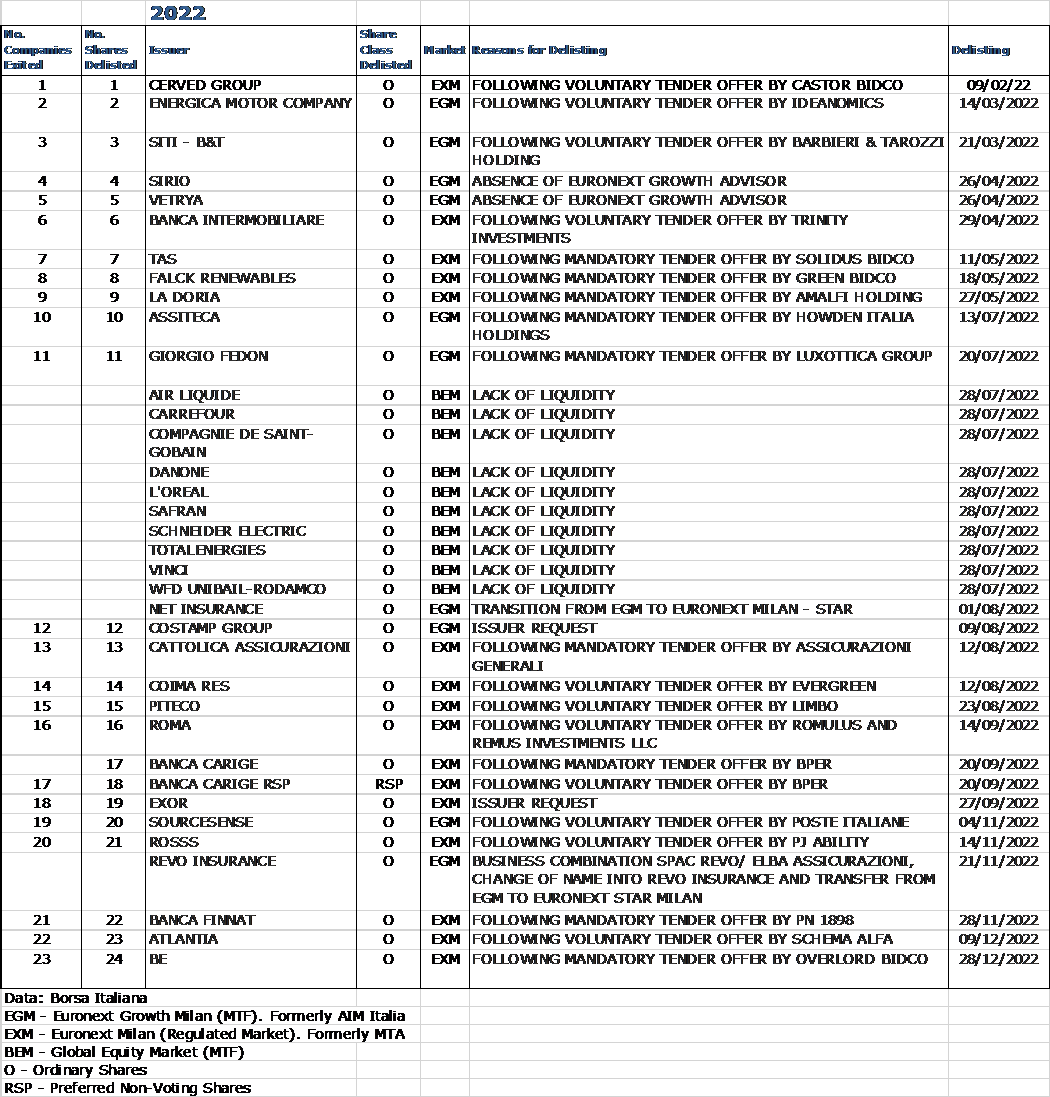

Tables in the following pages show Delistings from Regulated Markets and MTFs (January 2018–November 2023).

Data referred to previous years (starting from January 1995) available on Borsa Italiana’s website:

• Home page › About Us › Analysis and Statistics › All Historical Statistics

(look for Family: Historical statistics; Type: Delistings)

• www.borsaitaliana.it/borsaitaliana/statistiche/statistiche-storiche/revoche-202311.en_pdf.htm (last accessed 21 December 2023).

Figure 1: 2018

Figure 2: 2019

Figure 3: 2020

Figure 4: 2021

Figure 5: 2022