johndoe@gmail.com

Please find a PDF copy of this page here.

Name: Christoph Van der Elst

Date: November 2023

QUESTIONNAIRE ON DELISTING

The Netherlands

PART I. VOLUNTARY DELISTING

A delisting is deemed voluntary if it is initiated by the company or a shareholder.

1. Is voluntary delisting explicitly allowed by national laws or by jurisprudence?

Yes (X) No

Relevant provision:

Note that a removal of securities (delisting) is in the Euronext stock exchange provisions (not in national statutory law or jurisprudence, although case law confirms the validity).

The (decision of the) removal of the listing is taken by the Relevant Euronext Market Undertaking (here Euronext Amsterdam). According to Euronext Rulebook I (version of March 2023, Rule 6905/1) a class of securities can be delisted at the request of the issuer, the competent authority or Euronext. The local markets of Euronext can establish additional rules. Thereto, Euronext Book II: General Rules for the Euronext Amsterdam Securities Markets of May 2019 refers to Euronext Announcement 2004-41 which is (still) applicable.

The important threshold for starting a delisting process is the concentration of 95 per cent of (a certain type of) shares or 95 per cent of the depository receipts (Euronext Announcement 2004-41) in the hands of one or more shareholders acting in concert. Next, Euronext Announcement 2004-41 also offers the delisting option for (a certain type of) shares if the instruments ‘have also been listed for at least 12 months on another regulated and sufficiently liquid market that offers, in Euronext Amsterdam’s opinion, adequate safeguards for the protection of investors and the proper functioning of the market.’

2. If the answer to 1. is yes, who decides so?

BoD (X) GA Other (X)

Relevant provision:

If the request is issued by the company, the competent body is the board of directors (representing the issuer that can request for a delisting in accordance with Rule 6905 of Euronext Rulebook I (March 2023 edition)). Commonly Dutch companies have a two-tier board structure and the supervisory board must monitor that the board of directors is acting in the interest of the enterprise; therefore the involvement of the supervisory board in taking the decision of delisting is recommended as a delisting request is to be considered as an element of ‘general course of affairs’ that the supervisory board must supervise in accordance with Dutch company law (Article 2:141 Dutch Civil Code).

In court cases it was explicitly acknowledged by the Enterprise Chamber of the Court of Amsterdam that it is the board of directors decision to request a delisting (both cases were related to a delisting of a foreign (non-Euronext) stock exchange (A&D Pharma Holding, Court of Amsterdam (Enterprise Chamber), 31 January 2011, AA20110573, LJN: BP2986, JOR 2011/140, note J. Jitta and AAA, Court of Amsterdam (Enterprise Chamber), 28 March 2013, ECLI:NL:GHAMS:2013:BZ9658, JOR 2013/171, note J.Jitta).

It follows from the Euronext Amsterdam Announcement 2004-41 that also the shareholder(s) who hold(s) 95 per cent of (a certain type of) the shares or the depository receipts can request the delisting, if the issuer agrees to the delisting. The general Euronext Rulebook does not provide in a request of the supermajority shareholder(s), only of the issuer (or competent authority or Euronext). De facto it is a technical legal difference that does not cause difficulties.

3. What is the quorum requirement for the delisting decision of the competent organ?

All directors have access to and are expected to participate in board meetings. There are however no specific board quorum requirements. There are no other specific rules regarding the delisting decision.

If the request comes from the supermajority shareholder(s) (see Q 2), this/these shareholders must own more than 95 per cent of (a certain type of) the shares or the depository receipts (Euronext Announcement 2004-41). Note that in the Dutch Civil Code the different squeeze out regimes refer to a threshold 95 per cent of the issued share capital.

4. What is the majority requirement for the delisting decision of the competent organ?

At board level decisions are taken with a simple majority of the votes, unless the company’s organisational documents prescribe a higher majority or quorum. Each board member has one vote. However, the company's articles can provide that a managing director has multiple voting rights, provided that one managing director cannot cast more votes than all the other managing directors collectively.

For a request coming from a supermajority shareholder, see Q3, second par.

5. Do (minority) shareholders have statutory veto rights as to a delisting decision?

Yes No (X)

6. Should delisting take place within a specific timeframe after the relevant decision? Is there a specific period of time after the decision in which the delisting should be completed?

Yes (X) No

Relevant provision:

As a general rule the delisting takes place, 20 trading days after the decision of the delisting by Euronext Amsterdam.

The delisting is, according to 2004-41 of the Euronext Announcement allowed in 4 specific exit arrangements. In case of a public offer (squeeze-out, Article 2:359c Book 2 Dutch Civil Code (DCC)) or buyout arrangement (Article 2:92a/201a Book 2 DCC) a specific precedent procedure (with, in the former case a number of time related issues, like starting the squeeze out with a request thereto within three months after the end of the acceptance period of the bid) applies. For the other two grounds of delisting in the 2004-41 of the Euronext Announcement, the offer by the issuer and an arrangement accepted by Euronext Amsterdam, must be open for 20 trading days. With the exception of the public offer, all other exit schemes request an announcement in a press release, an advertisement in a national daily newspaper and in the Euronext Amsterdam Daily Official List.

In case of a public offer (Article 2:359c Book 2 DCC) the delisting takes place after the offer ends.

In the case of the buyout arrangement (Article 2:92a/201a Book 2 DCC) the delisting takes effect upon completion of the procedure.

In case of the offer by the issuer, the delisting takes place 20 trading days after the start of the purchase offer and for the other arrangements, the same number of days after the announcement in the press release, the advertisement in the financial press (daily newspaper) and Amsterdam Daily Official List of this accepted arrangement.

7. Should the delisting application give a full statement of reasons for the submission of such application?

Yes (X) No

Relevant provision:

According to the Euronext Rulebook (version of 2023, Rule 6905/1-6905/3) the delisting requested by the issuer must state the relevant grounds for removal (Rule 6905/3) and in case Euronext initiates the delisting the issuer is being informed and can respond to the intention of Euronext (Rule 6905/2 (i)) and Euronext publishes the conditions of removal (Rule 6905/2 (iv)). The common grounds that Euronext uses for delisting securities can be found in Rule 6905/1 para 2.

Indirectly: delisting follows almost always another event (offer, decision of supermajority shareholder, etc.) which is used as a trigger for the delisting decision and these procedures are accompanied with extensive reports. Further, these procedures, like squeeze out and supermajority offer must take place via filing a claim with the Dutch enterprise chamber.

8. Is it required that a competent authority approves the voluntary delisting?

Yes (X) No

Relevant provision:

Amsterdam Euronext (but not the supervisory authority AFM (Dutch Authority for the Financial Markets) may remove the securities at the request of the issuer. Rule 6905/1 states explicitly ‘may’. It is further clarified in Rule 6905/4 that the stock exchange Euronext Amsterdam has the option ‘not to remove Securities upon the Issuer’s request if such removal would adversely impact the fair, orderly and efficient functioning of the market’.

Conversely, Euronext Amsterdam can also delist the securities if requested to do so by the competent authority (AFM) according to Rule 6905/1 (iii). Amsterdam Euronext can be requested to do so when the issuer or beneficial owners are on the EU Sanction List or on the list of the Office of Foreign Assets Control (OFAC).

If the answer to 8. is yes, who is the competent authority?

Euronext Amsterdam.

If the answer to 8. is yes, does the competent authority has the competence to verify the reasons of delisting?

Yes (X) No

Relevant provision:

Euronext Rule 6905/4 indirectly gives Euronext Amsterdam this power of assessment (aforementioned in question 8). Further in Rule 6905/3 it is highlighted that the procedure for removal of the securities starts with a written request stating ‘the relevant grounds for removal.’ Consequently it will contain the reasons of delisting.

If the answer to 8. is yes, does the competent authority have any discretion? Can the competent authority impose additional terms for investor protection? Can the competent authority postpone the decision? If Yes, do you know whether this discretion has been used in the past?

Yes (X) No

Relevant provision:

It follows from the Rules 6905/4, 6905/3 and 69501/1 Euronext Rulebook. I am not aware whether this discretionary right has been used actively (meaning that Euronext Amsterdam rejected the request for delisting). From a recent court ruling it can be deducted that Amsterdam Euronext does carefully assess the request of a company/shareholder for delisting (Court of Amsterdam 3 March 2022, case C/13/714460 / KG ZA 22-177, ECLI:N::RBAMS:2022:1635).

9. In case of a voluntary delisting does the issuer have to make an offer to buy the shares of (dissenting) shareholders?

Yes (X) No

Relevant provision:

Note that there seems to be only one type of delisting, in casu when the company’s securities remain listed at another stock exchange, that the issuer makes this offer, when reading the first part of the Announcement 2004-41. Only in that particular case it is the issuer requesting the delisting which will provide in an exit mechanism for the shareholders signaling that the delisting from Euronext Amsterdam triggers their decision to sell. As it is the board of directors that requests the delisting, the position of the shareholders vis-à-vis the delisting – dissenting or not - is not considered. The other types of delisting in the first part of the Announcement 2004-41 refers to a request of the supermajority shareholder with the agreement of the company (aforementioned in Q 2 it was signaled that the Euronext Rulebook does not provide in this option – it must be the issuer - but the practice of the request by the supermajority shareholder(s) is well established). In light of the second part of Euronext Announcement 2004-41 there is another procedure provided whereby the issuer is making the offer.

The first part of Euronext Announcement 2004-41 addresses the issuer’s request as follows. ‘If the shares of a certain type or the depositary receipts for a certain type of share listed on Euronext Amsterdam’s stock market have also been listed for at least 12 months on another regulated and sufficiently liquid market that offers, in Euronext Amsterdam’s opinion, adequate safeguards for the protection of investors and the proper functioning of the market.’

The applicable exit mechanism for this kind of delisting is provided in the second part of Euronext Announcement 2004-41: ‘An offer by the issuer to buy the listed shares of a certain type or the listed depositary receipts of a certain type of share that remains open for a period of 20 trading days' (1).

In one delisting case in 2021, Euronext Amsterdam has accepted the delisting of an issuer that retained its listing at a non-European stock exchange making use of a procedure that resembles the buy-back of the shares by the issuer but it had a different legal setup. The shareholders could step voluntarily into a sales facility which was structured as follows. The shareholders of this issuer could transfer their shares cost-free to an intermediate bank, which facilitated the sale of such transferred shares on the foreign stock exchange. Proceeds of the sale of these shares were distributed to the beneficiaries upon receipt of the funds by the intermediate bank.

In another delisting case in 2019, this exit mechanism provided in the second part of Euronext Announcement 2004-41 (the issuer buys its listed shares) was used by the issuer whereas the first part of the Euronext Announcement 2004-41 seems to indicate that the exiting mechanism should have been launched by the supermajority shareholder. First, the latter shareholder passed the threshold of 95 per cent of the shares. Nevertheless and thereafter, it was the company that requested for a delisting making use of the exit mechanism of a buy back. After the delisting, the supermajority shareholder launched the statutory squeeze-out mechanism of Article 2:92a/201a DCC. The information note of the delisting provided in the details of the (reversed) process.

If the answer to 9 is yes, at what price should the offer be made? How is the price calculated?

In the aforementioned case of 2019 the price was determined by the (board of directors and supervisory board of the) issuer taking into account that the price was higher than the average stock price in the three and six months before the buy back was launched (approximately 5 per cent higher) and higher than the highest price that the supermajority shareholder had paid for the acquisition of the shares that resulted in passing the threshold of 95 per cent of the shares (6.5 per cent higher price).

Note that in the procedures preceding the delisting often raise difficult questions regarding the consideration for the shares. In short, in the corporate buy-out arrangement (Article 2:92a/201a DCC) the law provides that ‘the court determines the price of the shares to be transferred on a day to be determined by it. As long as and insofar as the price has not been paid, it will be increased with interest, equal to the legal interest, from that day until the transfer;’

10. Are there any restrictions due to the principle of maintenance of the share capital?

Yes No (X)

Relevant provision:

There are no other specific rules than those that generally apply related to the maintenance of capital for Dutch limited liability companies.

11. Does a (majority) shareholder or a third person has the right to offer to buy the shares of (dissenting/all) shareholders and relieve the issuer?

Yes (X) No

Relevant provision:

The common process before a delisting entails that a supermajority shareholder offers the other shareholders an exit. The issuer should not be relieved as it is not acquiring shares for obtaining a delisting. Article 2:92a/201a DCC states: He who as a shareholder for his own account provides at least 95 per cent of the issued capital of the public limited company, can bring a claim against the joint other shareholders for the transfer of their shares to the plaintiff. The same applies if two or more group companies jointly provide this part of the issued capital and jointly file a claim for transfer to one of them. Article 2:359c DCC offers the squeeze-out after a takeover.

Further in pre-wired back end structures (like triangular mergers) which are also used for obtaining full control over the company, it is not the issuer acquiring its shares.

See also Q 2 and 9.

12. In case of a voluntary delisting does the issuer or a third person have the obligation to publish a prospectus / informational document?

Yes No (X)

Relevant provision:

The voluntary delisting itself does not trigger the duty of publishing a prospectus or information memorandum. There will be a press release that commonly provides in detailed information with the timing of the delisting and the offered exit mechanism (which you also can qualify as an ‘informational document’). Note that there is an exemption of the statutory public offer rules for share buy backs (Article 56a (b) of the exemption regime of the Law on Financial Supervision (Vrijstellingsregeling Wft).)

The procedures taking place prior to the delisting (like a takeover) will often trigger such an information obligation.

13. Is an exit opportunity / mechanism that allows investors to exit their investments (e.g. sell – out right) available for shareholders in case of delisting? What are the relevant provisions (please provide translations)?

Yes (X) No

Relevant provision:

See Q 9 and 11.

14. Is there any specific provision on downlisting? If not, is downlisting allowed, and how does it take place?

A downlisting occurs when the shares are no longer traded on a regulated market (as defined by Union law) but on an MTF.

Yes No (X)

Relevant provision:

Downlisting is not separately addressed. Therefore I opine the regular rules apply: Euronext Rulebook I (version of March 2023, Rule 6905/1) and Euronext Announcement 2004-41 (Amsterdam) and that Euronext Amsterdam will in particular look after ‘adequate safeguards for the protection of investors and the proper functioning of the market’ (quote from Euronext Announcement 2004-41).

15. Is there any specific provision on market migration (delisting from a regulated market and listing in another)?

Yes (X) No

Relevant provision:

2004-41 of the Euronext Announcement addresses this issue: ‘If the shares of a certain type or the depositary receipts for a certain type of share listed on Euronext Amsterdam’s stock market have also been listed for at least 12 months on another regulated and sufficiently liquid market that offers, in Euronext Amsterdam’s opinion, adequate safeguards for the protection of investors and the proper functioning of the market.’

16. Is there any specific provision on voluntary delisting in case of increase of listing requirements by both the Law and Stock Exchange?

Yes No (X)

Relevant provision:

In theory it can be a reason for delisting if the company does not comply with the Euronext requirements. Amsterdam Euronext can make use of Rule 6905/1 para 2 a) that states that it can initiate a delisting in case of:

a) manifest failure of the Issuer to comply with the obligations imposed and the requirements set pursuant to the Rules or the Application Form;

It cannot be considered as a voluntary delisting.

17. Are there different rules on delisting for national and foreign listed companies?

Yes No (X)

18. Cold delisting is usually described as a transformation of a listed company resulting to its delisting, including especially the merger by absorption of a listed company by an unlisted company. What is defined as cold delisting in your legal order? Is there any specific provision on cold delisting?

There is no legal definition of cold delisting; cold delisting can be seen as restructuring measures under corporate law leading to the acquisition of (as good as) all the securities of the corporation by an acquiror. Thereafter, in a second phase a delisting request is initiated. There are no specific provisions for cold delisting. The applicable provisions depend on the specific restructuring measure; multiple procedures exist (pre-wired back end structures) (2). The procedures are especially envisaged in public take-overs which do not result in the acquisition of sufficient securities which allow for a squeeze-out following the take-over bid.

19. Does the merger of a listed company with a non-listed company lead to delisting? Is an exit opportunity available for shareholders? What are the relevant provisions? (please provide translations)

Yes No

It is one of the procedures that is being applied in case an acquisition offer does not result in the fulfillment of the conditions that can lead to a request for delisting (in short: a supermajority shareholder exceeding 95 per cent of the issued share capital). A merger can be initiated with a subsidiary of the offeror watering down the stake of the remaining shareholders under 5 per cent or a merger which shifts the remaining shareholders to the share capital of the (listed) offeror.

20. Does the successful completion of a mandatory bid give the right to delisting? If yes, are there any preconditions?

Yes (X) No

Relevant provision:

This is the process provided in Article 2:359c Book 2 DCC (transposition of the squeeze out procedure in the European Takeover Directive); the squeeze out after a successful take-over will allow the request for delisting.

21. Are there specific rules on delisting from an MTF?

Regarding the voluntary delisting there are, as far as I could ascertain, no specific rules.

However, there are specific rules related to delisting. First, the Law on Financial Supervision provides in Article 4:91c (see also Article 32 MiFID II):

1. Een beleggingsonderneming die een georganiseerde handelsfaciliteit of multilaterale handelsfaciliteit exploiteert, kan de handel in een financieel instrument niet opschorten, niet onderbreken of een financieel instrument niet van de handel uitsluiten, indien het financieel instrument niet aan de regels van de handelsfaciliteit voldoet, indien een dergelijke maatregel de belangen van de beleggers of de ordelijke werking van de markt aanzienlijk zou kunnen schaden.

…

3. De beleggingsonderneming die de handel in een financieel instrument en eventueel hiermee verband houdende afgeleide financiële instrumenten opschort, onderbreekt of van de handel uitsluit, maakt deze beslissing openbaar en stelt de Autoriteit Financiële Markten daarvan in kennis.

1. An investment firm operating an organized trading facility or multilateral trading facility may not suspend, interrupt or exclude trading in a financial instrument, if the financial instrument does not comply with the rules of the trading facility, if such action could significantly harm the interests of investors or the orderly functioning of the market.

…

3. An investment firm that suspends, interrupts or excludes trading in a financial instrument and any related derivative financial instruments shall make this decision public and inform the Dutch Authority for the Financial Markets thereof.

Note that similar rules exist for the market operator of a regulated market (as provided in MiFID II).

Second, different from the other Euronext markets (like Paris and Brussels), the Amsterdam Euronext market does not have a multilateral trading facility. However, according to the Dutch Authority for the Financial Markets there are 11 MTFs licensed holders (as of 20 November 2023, www.afm.nl/en/sector/registers/vergunningenregisters/handelsplatformen).

One them is Cboe Europe B.V. Its CBOE NL Rule Book provides the following rules for delisting of securities, serving as an example:

2.6.1.Cboe NL admits Cboe NL Traded Securities to trading on the Cboe NL MTF Equities where they have first been listed or admitted to trading or are under an application to be listed by or admitted to trading on an EEA or equivalent trading venue and are deemed eligible for trading on the Cboe NL MTF. The admission of a Cboe NL Traded Security to or removal from trading on the Cboe NL MTF Equities is at the discretion of Cboe NL and the admission or removal of any Cboe NL Traded Security from trading shall be communicated by a Trade Desk Notice.

…

2.12.7. An Issuer may request the cancellation of the admission of its Securities in writing. Such notice must be provided twenty (20) Business Days prior to the date requested for the cancellation.

2.12.8. Cboe NL will confirm the cancellation via Trade Desk Notice and by notifying a Regulated Information Service. Cancellation will not be agreed to until an Issuer has confirmed that all relevant legal and regulatory obligations, including those arising under these rules, have been complied with.

PART II. OBLIGATORY DELISTING

A delisting is deemed compulsory/obligatory, if it is initiated by a supervisory authority or a market operator without consent of the company.

22. What are the prerequisites for compulsory delisting by the competent national supervisory authority?

• Delisting by the market operator:

Delisting by the Amsterdam Euronext Market takes place in accordance with Rule 6905/1 of Euronext Rulebook (version of March 2023) according to which the appropriate grounds for delisting are:

a) manifest failure of the Issuer to comply with the obligations imposed and the requirements set pursuant to the Rules or the Application Form; or

b) the legal entity that has issued the Securities shall cease to exist pursuant to a liquidation, merger, dissolution (or equivalent corporate event in any jurisdiction);

c) the Issuer of the Securities has been declared bankrupt (or analogous procedure has been declared applicable in any jurisdiction); or

d) without prejudice to Rule 4403/2, in the opinion of the Relevant Euronext Market Undertaking, facts or developments occur or have occurred with regard to a Security which prevent the continued listing of that Security or which cause the Relevant Euronext Market Undertaking to believe that a fair, orderly and efficient market for a Security cannot be maintained; or

e) adequate clearing and/or settlement services for a type of Securities are no longer available; or

f) the removal of the Shares or other Securities into which they are convertible or for which they are exchangeable, as the case may be; or

g) facts or developments occur or have occurred in respect of an Issuer which in the opinion of the Relevant Euronext Market Undertaking is detrimental to the reputation of Euronext as a whole;

h) the Issuer or its beneficial owners are on the EU Sanction List or the list drawn up by the Office of Foreign Assets Control (OFAC).

The issuer is always provided with a response time before the decision is made (Rule 6905/2).

• Delisting by the Dutch Authority for the Financial Markets:

The AFM (Dutch Authority for the Financial Markets) can request the Court of Rotterdam to exclude a security from being traded after the AFM had signaled Euronext Amsterdam of a suspicion of market abuse or a take-over bid or in the interest of investors (Article 5:77e Law of Financial Supervision).

23. Which body has been designated as the competent authority, in particular regarding the power to require the removal of a financial instrument from trading pursuant to art. 69(2)(n) MiFID II?

The Dutch Authority for the Financial Markets.

24. What are the rules of the market that can justify a compulsory delisting imposed by market (art. 52 MiFID II)?

See Q 22, first bullet. Note that Article 5:32g of the Law of Financial Supervision must be considered (transposition of MiFID, Article 52, 1.):

Een marktexploitant kan de handel op een door hem geëxploiteerde gereglementeerde markt in een financieel instrument niet opschorten, niet onderbreken of een financieel instrument niet van de handel uitsluiten, indien het financieel instrument niet aan de regels van de gereglementeerde markt voldoet, indien een dergelijke maatregel de belangen van de beleggers of de ordelijke werking van de gereglementeerde markt aanzienlijk zou kunnen schaden.

A market operator may not suspend, interrupt or exclude trading in a financial instrument, if the financial instrument does not comply with the rules of the regulated market, if such a measure could significantly harm the interests of investors or the orderly functioning of the market.

25. Have any of the voluntary or obligatory delisting requirements above changed materially since 2010 (e.g., due to a legal decision or amendment of the regulations)?

As Euronext Amsterdam makes use of the Euronext Announcement 2004-41 from 2004, there are no major changes in the delisting requirements.

The mandatory delisting rules have been updated when transposing MiFID II as well as considering Commission implementing Regulation (EU) 2017/1005 of 15 June 2017 laying down implementing technical standards with regard to the format and timing of the communications and the publication of the suspension and removal of financial instruments pursuant to Directive 2014/65/EU of the European Parliament and of the Council on markets in financial instruments, Pb. L nr. 153, 16 June 2017.

PART III. GENERAL QUESTIONS (if not already answered)

26. How are dissenting shareholders protected in voluntary delisting?

The target company, majority shareholder and the minority shareholders must observe the standards of reasonableness and fairness towards each other (Article 2:8 DCC). The target company and the majority shareholder must exercise due care towards the interests of the stakeholders, including the minority shareholders (still present after the offer/in a delisting process). This may entail for directors and supervisory directors of the target company that they ensure that the interests of the minority are not disproportionately or unnecessarily harmed. The court of Amsterdam (Enterprise Court) decided in the Shell/Trafalgar case (20 December 2007, JOR 2008/36 ) that the structure of the merger conflicted with the reasonableness and fairness towards the minority shareholders. The structure provided in a nominal value of the shares that was very (unreasonable) high. Consequently, the minority shareholders would receive cash and no shares in the merged company. The payment in cash and the determination of the amount were lacking sufficient safeguards protecting the minority shareholders, like for example the determination of the price by and independent expert. As a result, the court ruled that the interests of the minority shareholders were disproportionately disadvantaged.

In addition, an impermissible entanglement of the interests of the bidder as a major shareholder and the interests of the minority shareholders must be prevented. Following the Versatel ruling of the Dutch Supreme Court, the interests of the minority shareholders can be taken care of by installing one or more of the bidder independent supervisory directors, who may, where appropriate, have a right of veto over decisions that potentially disproportionately affect the position of the minority shareholders (such as entering into material intra-group transactions between bidder and target company). The prewired restructuring was already approved by - at the time of this prewired restructuring decision - independent (from the bidder) board of directors as well as supervisory board of the issuer. (this part is largely taken from and a translation of C. de Brauw, Overnames van beursvennootschappen, Kluwer, Deventer, 2017, 749-750).

Note 1: This is specifically regarding the delisting as such; voluntary delisting, as previously addressed, follows mostly another procedure (like an offer) via which the shareholders are protected. Insofar that shareholders are not deprived of their shares (which is for instance the case in the squeeze out), these offers document for the shareholders also the consequences of the procedure, i.e. the delisting.

Note 2: There is a discretionary right of Amsterdam Euronext in Rule 6905/4 Euronext Rulebook March 2023: the Relevant Euronext Market Undertaking may decide not to remove Securities upon the Issuer’s request if such removal would adversely impact the fair, orderly and efficient functioning of the market (and in Announcement 2004-41 it sounds: ‘Securities will not be delisted if Euronext Amsterdam is of the opinion that this would be detrimental to the protection of investors or the proper functioning of the market.’

Note 3: The Enterprise Chamber of the court of Amsterdam was addressed in the delisting process of A&D Pharma Holding by a group of minority shareholders. A&D Pharma Holding was a Dutch public limited liability company of which the main shareholder had 30 per cent of its shares via the issuance of certificates of shares placed in the UK market (LSE), not via Euronext Amsterdam. Citybank obtained the shares and issued Global Depository Receipts (GDR). However, there was never a larger market and interest in these GDR. After some years the extra-ordinary meeting of A&D Pharma Holding discussed the termination of the listing and the deposit agreement and A&D Pharma Holding offered the acquisition of the GDR (at a significant lower price than the issuance price) or to convert the DGR in shares of A&D Pharma Holding (although these were not listed). Some of the GDR-holder launched a request (based on the specific rules to take the case to the Enterprise Chamber (i.e. that there is reason to doubt whether the company follows an appropriate policy or state of affairs) to forbid the company A&D Pharma Holding to delist and forbid the majority shareholder to vote for the delisting item at the special general meeting of shareholders (as the articles of association require a shareholder vote for delisting). The court rejected all claims of the shareholders (Court of Amsterdam (Enterprise Chamber), 31 January 2011, AA20110573, LJN: BP2986, JOR 2011/140, note J. Jitta). Nevertheless, there seems to be room for the shareholder to address the court. The shareholders can take legal action against the market operators revocation decision. A recent court case (Court of Amsterdam 3 March 2022, case C/13/714460 / KG ZA 22-177, ECLI:N::RBAMS:2022:1635) seems to confirm this view (the court dismissed all the claims of the shareholder after assessing each request which would have led to maintain the listing of the shares).

27. What are the sanctions in case of a breach of the delisting rules?

There are no specific legal sanctions in case of a breach of delisting rules insofar it relates to the specificities of the delisting itself. Note that general contract law or tort law can be applied. A recent court case (Court of Amsterdam 3 March 2022, case C/13/714460 / KG ZA 22-177, ECLI:N::RBAMS:2022:1635) seems to confirm this view (the court ruled that Euronext committed no breach).

Euronext itself can take action in case the issuer is violating any of the Euronext Rulebook rules in accordance with rule 9301/1, which include the termination of the membership.

28. Is there a special duty of loyalty (for the board or, if applicable, the shareholders) imposing further restrictions in connection with a delisting?

There is no special duty of loyalty for the board other than those referred to in Article 2:8, see Q 26.

29. How are shareholders protected in obligatory delisting?

There are no specific rules related to the protection of shareholders in case Euronext Amsterdam decides to delist the securities. In the aforementioned court case C/13/714460 / KG ZA 22-177 the plaintiffs also refer to the fact that Euronext violated Article 5:32g of the Law of Financial Supervision (see Q 24). However it was the issuer that requested the delisting, not Euronext Amsterdam. The court stated: ‘The claim is therefore not admissible on this ground neither’. It seems to indicate that if Euronext Amsterdam delists the securities, shareholders have a ground to refer this matter to the court.

30. Have shareholders successfully challenged delisting decisions in the past? If Yes, could you provide any names of cases?

As far as I could ascertain, there are no cases.

31. How is the issuer protected in (obligatory) delisting?

The issuer is always provided with a response time before the decision is made (Euronext Rule 6905/2).

Also, there is Euronext Rule 6906/1 (edition March 2023) that provides that ‘An Issuer may appeal against the decision of the Relevant Euronext Market Undertaking to remove in accordance with National Regulations.’

32. How does insolvency and restructuring of a listed company affects delisting? Specifically: a) Does the initiation of formal insolvency (liquidation) procedures automatically trigger mandatory delisting? b) Does the initiation of formal restructuring / reorganization procedures automatically trigger mandatory delisting? c) If the above scenarios do not automatically trigger mandatory delisting, what else are the implications? d) Please give empirical information (if available) on the treatment of insolvent listed firms by trading venues in your jurisdiction e) What are the relevant provisions (please provide translations)?

Delisting by the Amsterdam Euronext Market takes place in accordance with Rule 6905/1 of Euronext Rulebook (version of March 2023) according to which the appropriate grounds for delisting are:

...b) the legal entity that has issued the Securities shall cease to exist pursuant to a liquidation, merger, dissolution (or equivalent corporate event in any jurisdiction);

c) the Issuer of the Securities has been declared bankrupt (or analogous procedure has been declared applicable in any jurisdiction); or ….

Therefore the questions a) to c) and e) are that Euronext Amsterdam will delist the securities of the issuer. It is not common that listed companies of Euronext Amsterdam are declared bankrupt. Between 2013 and 2023 there were two cases, both in 2017: Royal Imtech and Macintosh Retail. Recently, (at the time of writing) in 2023, there were also a significant number of voluntary liquidations of SPACs. Other data can be found in Q 35.

33. Do relevant courts have the power to examine the delisting reasοns on the merits?

In Q 26, note 3 reference is made to several cases from which it follows that courts can be addressed and assess the reasons of the delisting.

34. What are the legal consequences of delisting: a) on shares, b) on shareholders, c) on the issuer?

a) The main consequence of delisting on shares is that the shares can no longer be traded on the market. It can be that the securities are still traded on another market (in case of dual or multiple listings), or that all shares have been acquired in the bid, or, as the case A&D Pharma Holding remain in the hands of the remaining shareholders.

b) See a) After delisting the listing requirements no longer apply, which has a deregulatory effect on the company. However, corporate law (and its protective framework for shareholders) is still applicable.

c) none. (obviously the company is no longer submitted to the specific requirements of the listed entity (like specific disclosure rules, market abuse rules etc)).

35. Are there any statistical data on delisting in your Country? If yes, please provide further details. Are there any statistical data, or evidence, on downlisting in your Country? If yes, please provide further details. Are there any statistical data, or evidence, on delisting from an MTF in your Country? If yes, please provide further details.

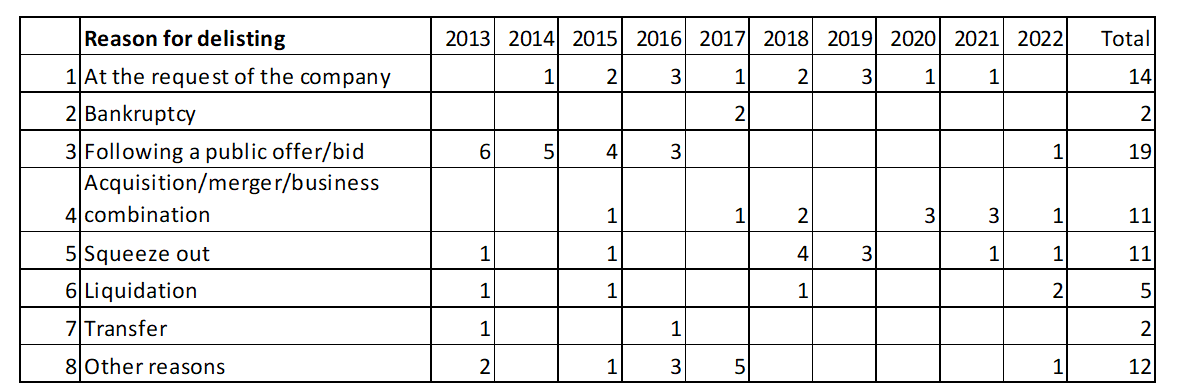

Table 1 provides the list of the number of delistings, the year of delisting and the reason of delisting according to the data provided in the yearly Factbook report of Euronext. Note that the reasons are not always fully developed. Whilst Euronext reports 11 squeeze outs (followed by a delisting), in fact also the requests of the company for a delisting (reason 1) contain a number of squeeze outs (according to book 2:359c Dutch Civil Code) and the 2016 transfer was an upgrade of a company listed at the former Alternext Amsterdam to Euronext Amsterdam.

There are no further data of downlistings or delistings from an MTF as far as I could ascertain.

Table 1: Number and reason of delistings (from Euronext Amsterdam) (2013-2023)

Own research based on Factbook Euronext (yearly edition)

36. More specifically, how many cases of voluntary delisting and / or obligatory delisting by the competent national supervisory authority have there been since MiFID I entered into force in 2007? Please also provide the main reasons for mandatory delistings, if available.

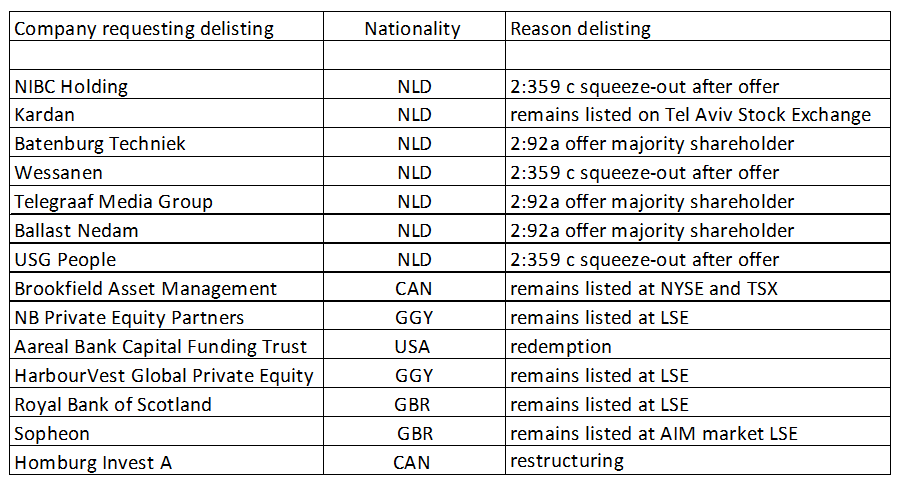

There are 14 companies that exited Euronext and were classified as delistings ‘at the request of the issuer’ (Table 1). 7 companies were Dutch, 7 companies were foreign companies (Table 2). Hereafter follows the reasons of the delisting. All Dutch companies are delisted in the aftermath of a bid by the supermajority shareholder or after a take-over followed by a squeeze-out but one, Kardan which remained listed on the Tel Aviv Stock Exchange. The foreign companies were all delisted from Amsterdam Euronext but maintained their listing at another stock exchange but two companies. One company was delisted due to insolvency/restructuring which was handled in Canada (were the company had its statutory seat), of the other company all securities were redeemed.

__________________________

(1) here is one other mechanism that Euronext Announcement 2004-41 offers but it results more than likely in a statutory public offer: ‘An arrangement that meets Euronext Amsterdam’s requirements regarding the protection of investors and the proper functioning of the market if and insofar as the Netherlands Authority for the Financial Markets (Autoriteit Financiële Markten) has granted full or partial dispensation from the rules regarding offers. Such an arrangement must specify that (i) it applies to all remaining shares or depositary receipts for shares of a certain type, (ii) the offer shall remain open for 20 trading days, (iii) the offer is based on the exchange price and/or the intrinsic value of the securities prior to the initial announcement of the exit arrangement.’

(2) See J Barneveld, ‘De achterkant van het openbaar bod’ (2019) No 5 Maandblad voor Ondernemingsrecht 155.